Are Residential Developers Building for the Buyers They Think Exist?

House Buying Behaviours Are Changing.

For decades, residential property has benefited from one of the strongest assumptions in British consumer life: buying a home is not only desirable, but rational. It has been treated as a marker of adulthood, security, family progress and long-term wealth creation. For developers, this assumption has often created a relatively straightforward commercial logic: build homes in viable locations, meet planning requirements, produce an acceptable specification, price against comparables, and trust that demand will exist.

That logic is no longer enough.

Today’s housing market is not suffering from a simple lack of desire. Many people still want to own. The deeper issue is that ownership is now being judged through a more complex lens: affordability, risk, lifestyle flexibility, energy performance, mortgage exposure, job security, alternative investments, family formation, work patterns and personal values. Buyers are not just asking, “Can I afford this home?” They are increasingly asking, “Is this the best use of my money, my time and my future optionality?”

This creates a difficult but important challenge for the residential development market. If buyers are becoming more cautious, analytical and segmented, then developers cannot rely on broad assumptions about “families”, “downsizers”, “commuters” or “first-time buyers”. They need a sharper understanding of what different buyer groups are actually willing to invest in before land, planning, product mix, layout, specification and sales strategy are fixed.

The buyer has become more analytical, more selective and more risk-aware.

One of the clearest shifts in buyer behaviour is the move from emotional browsing to active filtering. Mullucks describes today’s buyers as “more analytical, more cautious, and more selective”, noting that people are comparing properties earlier, judging value more quickly and filtering out homes that lack clear information on price, condition or suitability. Buyers are also asking more detailed questions around running costs, energy efficiency, maintenance and future works.

This matters because the old sales journey assumed persuasion could happen later: at the viewing, during negotiation, through the agent, or after a buyer had already emotionally committed. Now, many homes are being rejected before a viewing is even booked. The property listing, the development story, the EPC rating, the floorplan, the running cost assumptions and the perceived “future life” of the home all form part of an earlier decision-making filter.

Concentric Property makes a similar point from a product-feature perspective. Its 2025 buyer trends report identifies energy efficiency, outdoor space and flexible layouts as increasingly important buyer priorities. Energy efficiency is framed not just as a nice-to-have, but potentially a “dealbreaker”, while flexible space is linked to the way modern buyers no longer think purely in traditional room categories.

For residential developers, this is a strategic warning. Buyers are not simply comparing square footage, location and bedrooms. They are comparing risk, adaptability, monthly cost, lifestyle fit and long-term usefulness. A three-bedroom house is no longer just a three-bedroom house. It might be a home office strategy, a future nursery strategy, a multigenerational care strategy, a rental resilience strategy, or a “stretch once, don’t move twice” strategy.

Affordability has shifted the meaning of value.

The biggest behavioural driver remains affordability. But affordability is no longer only about the headline house price. It is about the full cost of entry: deposit, mortgage rate, stamp duty, legal fees, energy bills, service charges, maintenance exposure and the opportunity cost of tying up capital.

The Building Societies Association’s 2025 research found that 59% of renters aged 25–44 expected to own a home by now, while 33% of renters in that age group want to buy but do not think they will ever be able to. The same research found that 67% of first-time buyers see raising a deposit as the biggest obstacle, 61% cite mortgage affordability, and 48% cite accessing a large enough mortgage. Only 15% of the overall population thought it was a good time to buy a home.

That is a profound mindset shift. It suggests that the aspiration to own remains strong, but the route to ownership feels increasingly blocked, delayed or compromised. In behavioural terms, the buyer is still emotionally interested but financially defensive.

Recent market data supports this more cautious picture. Halifax reported that the average British home value edged down in May 2026, with annual growth of just 0.5%, while affordability pressures, borrowing costs and consumer confidence continued to shape activity. Industry commentators quoted by The Negotiator argued that buyers remain engaged, but are becoming more selective, more price-sensitive and more cautious in response to higher mortgage repayments and wider cost-of-living concerns.

Rightmove’s May 2026 data offers a more resilient counterpoint. Sales agreed were down 4% year-on-year but still 2% higher than the same period in 2024, suggesting that many buyers are still proceeding where affordability allows. First-time buyer sales were also only 1% lower than 2024.

This is where the market becomes nuanced. It is not that demand has disappeared. It is that demand is conditional. Buyers still move, but the threshold for action is higher. They need more reassurance, clearer value, stronger justification and a better fit between the home and their future life.

Stamp duty and upfront costs are changing what people choose to buy.

The cost of buying has become a behavioural force in its own right. BuyAssociation’s June 2026 article, citing Connells Group analysis, reported that a record 30% of first-time buyers in England are now buying homes above £300,000 and therefore paying Stamp Duty. That figure has doubled over the past decade. In London, 78% of first-time buyers now buy above £300,000 and pay Stamp Duty, with an average bill of £12,690.

This does not just make buying harder. It changes what people buy.

If moving is expensive, buyers may stretch for a larger home earlier so they do not have to move again soon. BuyAssociation notes that more first-time buyers are purchasing later in life and looking for homes that can meet their needs for longer. In London, half of first-time buyers now purchase homes with three or more bedrooms, compared with 43% a decade ago.

This behaviour has major implications for development strategy. The “starter home” may not be what developers assume it is. For some buyers, a small, compromised first step may feel financially irrational if transaction costs make future moves expensive. Instead, they may prefer a home that can absorb life changes: remote work, children, ageing parents, lodgers, home businesses or future resale flexibility.

That means developers should be asking more precise questions much earlier: Are buyers looking for affordability now or durability over time? Are they trying to minimise monthly payments or avoid future transaction costs? Are they buying for lifestyle, investment, family resilience, or emotional security? Each answer points to a different product strategy.

Renting is no longer just a waiting room before ownership.

The traditional UK housing ladder narrative treats renting as temporary: a stage people pass through before buying. That is becoming less reliable.

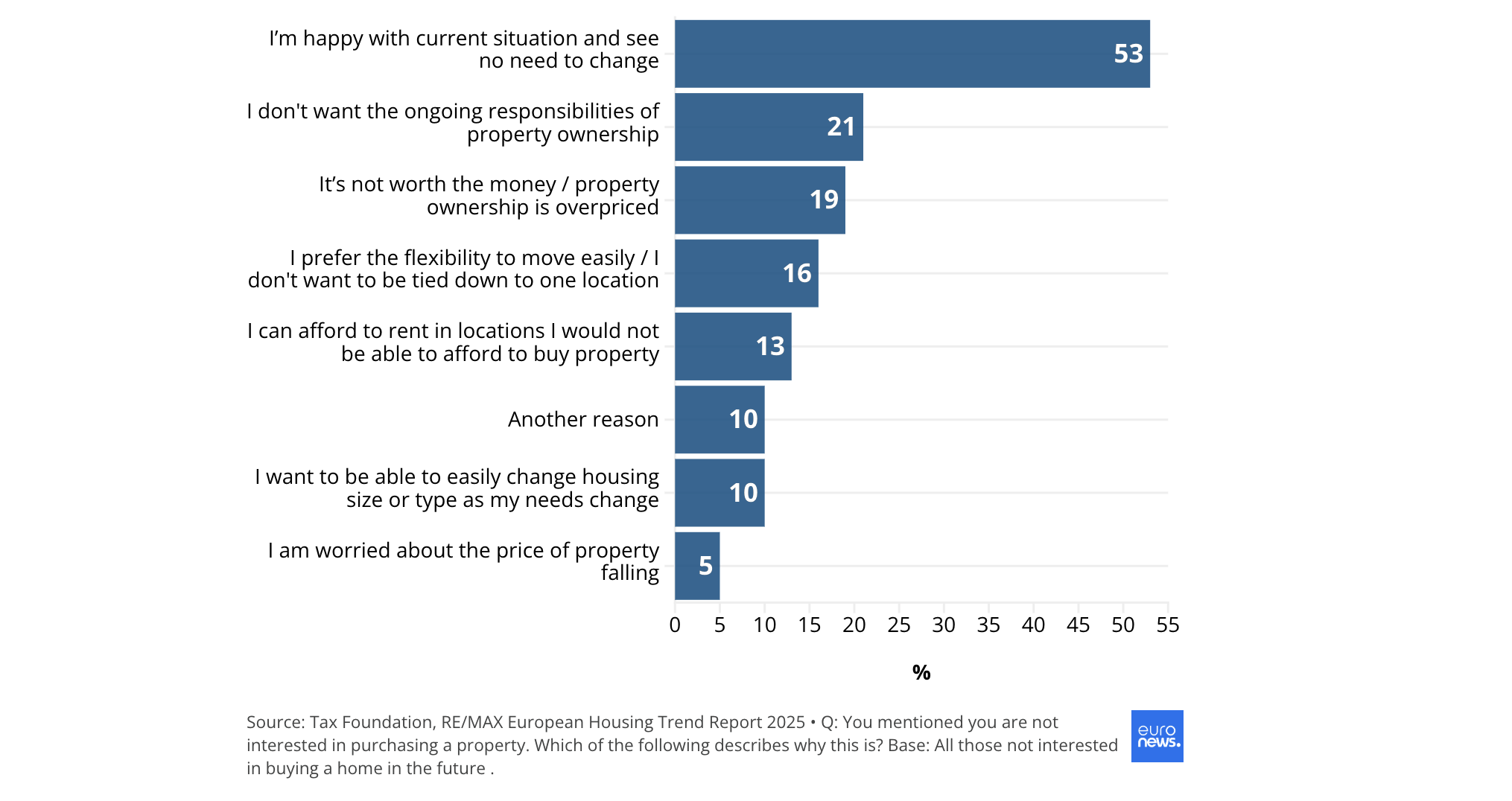

The BSA’s “Generation Stuck” findings show that many renters still want to own, but feel unable to do so in the timeframe they expected. Meanwhile, Euronews reported on the RE/MAX European Housing Trend Report 2025, which found that across 23 European countries, 44% of non-homeowners either believe they will never be able to buy or are not interested in buying. The UK figure was also 44%, in line with the European average.

There are two different behaviours inside that number. One is forced exclusion: people want to buy but cannot. The other is strategic opting out: people are less convinced that buying is necessary, desirable or worth the sacrifice.

In countries such as Germany and Austria, renting is more culturally accepted and supported by stronger tenant protections. Euronews notes that Germany and Austria have among the highest combined shares of non-homeowners who either doubt they will buy or are not interested, partly reflecting the cultural normality of renting.

The UK is not Germany. Ownership still carries strong emotional and financial weight here. But the comparison matters because it reveals a broader cultural possibility: once renting becomes more acceptable, more secure or more financially rational for certain groups, ownership has to compete harder. It can no longer rely solely on social expectation.

The Renters’ Rights Act 2025 may also shape this equation over time. While its effects are still unfolding, Reuters reported that regulatory pressure linked to the Act is expected to contribute to rental supply constraints as some landlords exit the market, with urban rents forecast to rise faster than home prices in 2026.

This creates a paradox. Renting may become more culturally acceptable for some, but also more expensive and competitive. Buying may remain desirable, but harder to access. Developers who understand this tension can position homes not simply as assets, but as solutions to instability, uncertainty and life-stage friction.

The “home as investment” belief is being challenged.

One of the most important emerging debates is whether a home is still the best long-term investment.

Historically, UK property has been treated as a safe wealth-building mechanism: tax-efficient capital growth, leveraged exposure to an appreciating asset, forced saving through mortgage repayment, and eventual security in retirement. That argument has not disappeared. For many households, ownership still offers long-term stability, protection from rent increases, control over the home environment and a route to building equity.

But the opposing view is becoming more visible. In online personal finance communities, the rent-versus-buy debate increasingly focuses on opportunity cost. One Reddit discussion asks whether buying is “even worth it from a financial perspective anymore”, arguing that high mortgage interest, carrying costs and modest historic appreciation can make the numbers less compelling than investing elsewhere.

Another UK-focused Reddit discussion frames renting and investing the difference as a potentially faster route to wealth accumulation, because stamp duty, deposits and mortgage interest can absorb capital that might otherwise compound in markets. A separate FIREUK thread captures the counterpoint neatly: buying a residence is not only a financial investment, but “an investment in lifestyle”, privacy and security from being forced to move.

These online conversations should not be treated as representative data. They are signals, not statistics. But they are useful because they reveal how financially literate buyers are reframing the decision. The home is being compared against stocks and shares ISAs, pensions, crypto, global mobility, career flexibility, family support, lifestyle consumption and renting in better locations.

Fortune’s reporting on Gen Z in the US points to a similar psychological pattern. It describes younger people who feel homeownership is unattainable, and links this to “financial nihilism”, riskier investments and changing attitudes to work and spending. The US market is different from the UK, but the underlying cultural signal is relevant: when traditional financial milestones feel unreachable, people do not simply wait patiently. They redirect money, effort and identity elsewhere.

For developers, this is not just a macroeconomic issue. It is a proposition issue. If buyers are asking whether homeownership is worth the trade-off, then the product has to answer that question.

Energy efficiency is becoming a financial, emotional and lifestyle signal.

Energy efficiency is a good example of how buyer value is becoming more layered.

Rightmove’s 2025 Greener Homes Report found that 46% of properties for sale and 58% of rentals are now rated EPC C or above. It also found that average annual energy bills range dramatically by EPC rating: £571 for EPC A homes compared with £6,368 for EPC G homes.

This turns energy performance into more than a sustainability claim. It becomes a cost-of-living proposition, a mortgage confidence factor, a comfort benefit and a resale signal.

Yet the same report shows the complexity of consumer behaviour. Rightmove found that 84% of people say EPC ratings matter, but half of homeowners and nearly two-thirds of renters do not know their current property’s rating. Cost savings dominate as a motivation for green improvements, while 37% of homeowners say EPC ratings will not influence their next purchase.

This is precisely why developers need deeper research. The existence of a trend does not automatically tell you how to design for it. Some buyers will pay more for lower bills and future-proofing. Some will like the idea but not understand the value. Some will prefer visible lifestyle upgrades over hidden performance improvements. Some will only care if the benefit is translated into monthly savings, mortgage affordability, comfort or resale resilience.

A product strategy approach would not simply say, “Buyers want energy efficiency.” It would ask: Which buyers? In what language? At what price premium? With what proof? Against which alternative trade-off?

The market is not one buyer. It is multiple competing buyer logics.

The danger for residential developers is designing for an averaged buyer who does not really exist.

Today’s market contains multiple buyer mindsets operating at once:

The security buyer still sees ownership as protection from instability. They want control, permanence, privacy and a home they cannot be asked to leave.

The financially defensive buyer wants to own, but is acutely aware of mortgage exposure, interest rates, stamp duty, maintenance and resale risk.

The strategic renter may be able to buy, but prefers flexibility, liquidity and investment elsewhere — at least for now.

The future-proofing buyer is willing to stretch for a home that can support the next decade, not just the next two years.

The quality-of-life buyer places high value on light, outdoor space, flexible rooms, walkability, schools, community, wellbeing and everyday experience.

The yield-conscious investor judges residential property through rental demand, regulatory pressure, capital growth, energy standards and liquidity.

The values-led buyer cares about sustainability, local identity, material quality, community impact and whether a development feels considered rather than generic.

These groups may overlap, but they do not buy in the same way. They do not need the same evidence. They do not respond to the same marketing. They do not value the same floorplan. They do not make the same compromises.

This is where residential development often lags behind sectors like product, transport, technology and consumer goods. In those industries, upfront consumer segmentation, proposition testing, journey mapping and concept validation are core parts of development. Teams explore what people value, what they reject, where willingness to pay sits, how behaviours are changing, and which product attributes create preference.

In property, too much of that thinking still happens late. Once the site, planning, unit mix and design direction are already largely fixed.

The developer risks building supply for an outdated demand model.

The residential market has traditionally been supply-constrained, which can make developers feel protected. If housing is undersupplied, surely buyers will come?

But undersupply does not remove the need for product-market fit. It simply hides weak product-market fit for longer.

When buyers become more cautious, weaker propositions are exposed. Homes that do not clearly justify their price, lifestyle benefit or future value become harder to sell. Developments that rely on generic lifestyle language struggle to stand out. Specifications that look good in planning but fail to answer real buyer anxieties become commercial risk. Unit mixes based on historic demand may miss emerging behaviours around later-life first-time buying, hybrid work, multigenerational living, downsizing, rental competition or energy performance.

Savills’ June 2026 update shows the market softness clearly: Nationwide house prices fell by 0.6% in May, annual growth slowed to 1.7%, and surveyors reported low levels of new buyer enquiries alongside expectations of further price reductions. Yet mortgage approvals reached a 15-month high in April, again reinforcing the mixed picture: demand exists, but it is cautious, conditional and highly sensitive to confidence.

That is exactly the kind of market where better upfront strategy matters. When confidence is high, many products sell. When confidence is fragile, the best-understood products sell better.

What a product strategy approach would change

A product strategy approach to residential development would not replace planning, architecture, valuation or sales. It would strengthen them.

It would begin by treating the home as a product, the development as a portfolio, and the buyer as a segmented consumer with competing needs, constraints and motivations.

Before planning and construction, developers should be asking:

Who are the most commercially realistic buyer groups for this site — not in broad demographic terms, but in behavioural terms?

What are they trying to achieve by buying: security, investment, family growth, lifestyle upgrade, lower running costs, flexibility, status, community, retirement, income, or escape?

What are they afraid of: overpaying, future maintenance, resale weakness, mortgage stress, poor energy performance, lack of flexibility, isolation, service charges, poor transport, or buying too soon?

What are they willing to pay more for, and what do they expect as standard?

What would make them reject the development before viewing?

How should the unit mix, layout, specification, visualisation and sales story change in response?

This kind of work can influence real development decisions: number of bedrooms, flexible room design, storage, parking, outdoor space, EPC ambition, heating systems, material choices, communal features, visual language, launch timing, pricing strategy and sales collateral.

It can also help developers avoid a common mistake: treating marketing as the solution to a product problem. If the buyer proposition is weak, better brochures will not fix it. If the unit mix is wrong, better CGI will only make the mismatch more visible.

There is no single answer, and that is the point.

The future of house buying behaviour will not resolve into one clean story.

Homeownership will remain deeply desirable for many people. Renting will become a more deliberate lifestyle and financial strategy for others. Some buyers will stretch to buy bigger and move less often. Some will delay. Some will redirect capital into investments. Some will buy for emotional security even when the spreadsheet is marginal. Some will continue to see property as the most tangible route to wealth. Others will see it as an expensive, illiquid, over-romanticised asset.

The mistake is assuming one of these views is “the market”.

The opportunity for residential developers is to recognise that buyer demand is becoming more fragmented, more informed and more conditional. People are still willing to invest in homes, but they are scrutinising what that investment gives them in return: financially, emotionally, practically and socially.

That makes consumer understanding a commercial necessity, not a marketing exercise.

The developers who win will not simply build more homes. They will build sharper propositions around the lives, anxieties and ambitions of the people expected to buy them. They will research before they design. They will test before they commit. They will understand willingness to pay before specification is locked. They will translate macro trends into site-specific product choices.

The residential development industry does not need to become less property-led. It needs to become more buyer-literate.

Because in a market where homeownership is no longer an unquestioned default, the most valuable question is not “What can we build here?”

It is: “Who is this genuinely worth investing in for, and why?”

Ready to activate what you’re building next?

Whether you need to create immediate sales momentum, understand your future buyer more clearly, or shape a stronger long-term development pipeline, Lexwell-Partners helps turn property opportunities into commercially sharper activation systems.

From focused sprint activations that help buyers see the finished life sooner, to consumer strategy that uncovers who your audience really is, to pipeline growth strategy that brings clarity across future sites, we help developers move from project-by-project marketing to more confident, market-led growth.

Have a development, portfolio or opportunity you need to bring to life?

Let’s shape it, visualise it and activate it.

Get in touch with Lexwell-Partners to explore how we can support your next activation.